Having good credit opens doors: better loan terms, lower interest rates, apartment approvals, and even job opportunities. But what if you’re starting from zero?

In this article, you’ll learn exactly how to build credit from scratch, step by step—even if you’ve never had a credit card or loan before.

What Is Credit, and Why Does It Matter?

Your credit score is a number (usually between 300 and 850) that shows how reliable you are with borrowed money.

Lenders, landlords, and even some employers use it to decide:

- Can they trust you to pay on time?

- Are you financially responsible?

- Should they offer you better rates or terms?

Building credit early—even with small amounts—sets you up for long-term financial success.

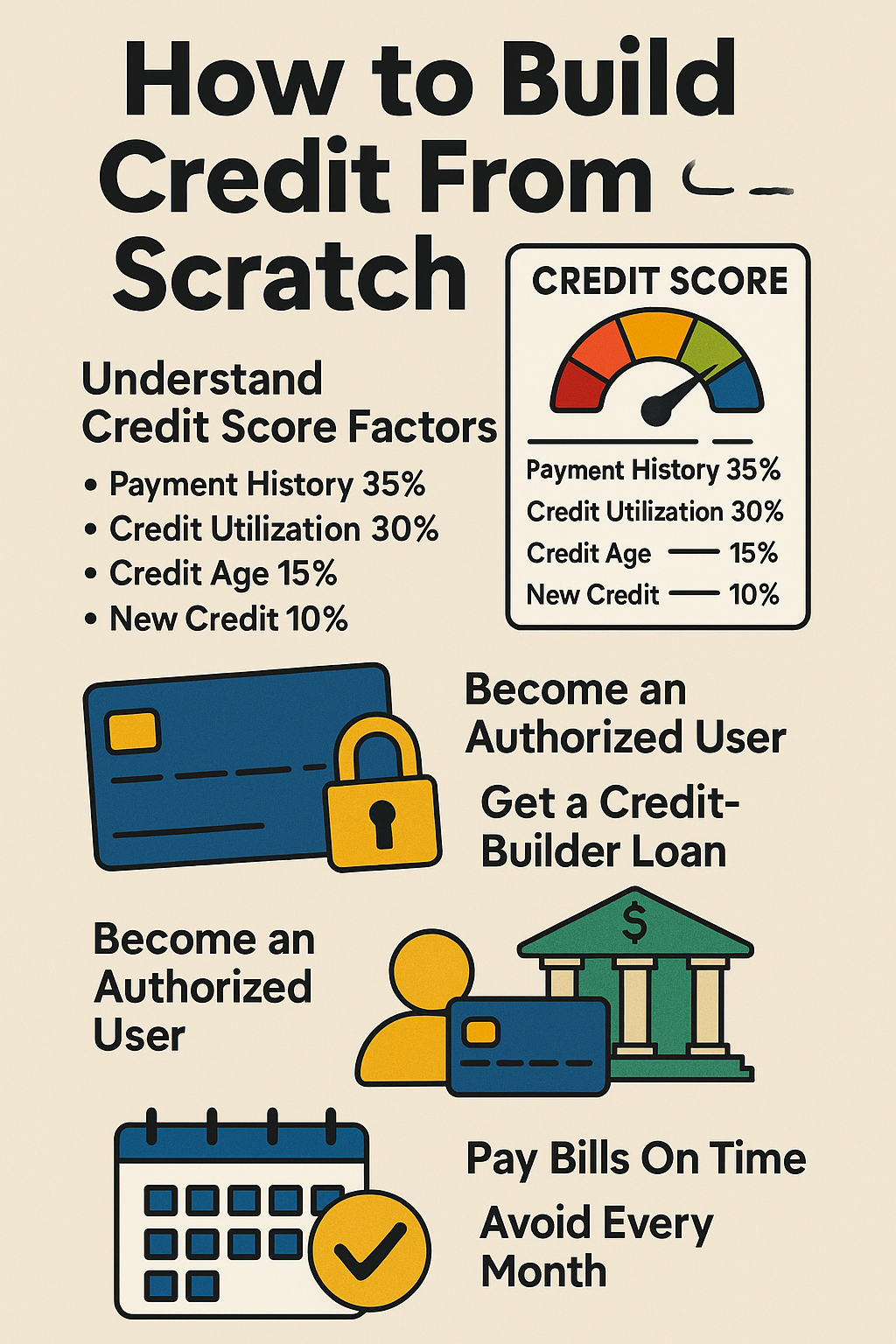

Step 1: Understand What Affects Your Credit Score

The most common scoring model is FICO, and it’s based on:

| Factor | Weight | Description |

|---|---|---|

| Payment history | 35% | Do you pay bills on time? |

| Amounts owed (utilization) | 30% | Are you using too much of your credit? |

| Length of credit history | 15% | How long have you had credit? |

| Credit mix | 10% | Do you have different types of accounts? |

| New credit | 10% | Have you applied for many accounts recently? |

Step 2: Open a Secured Credit Card

A secured credit card is the best way to start building credit with no history.

How it works:

- You put down a deposit (e.g., $200)

- That deposit becomes your credit limit

- You use the card and pay it off monthly

Pro tip: Only use 10–30% of your limit each month and always pay in full.

Step 3: Become an Authorized User

Ask a family member or trusted friend to add you as an authorized user on their credit card.

- You don’t need to use the card

- Their payment history and credit age will show on your report

- Choose someone with excellent credit and no late payments

This can give your score an early boost.

Step 4: Open a Credit-Builder Loan

Many banks or credit unions offer credit-builder loans.

How it works:

- You make small monthly payments into a locked savings account

- When the loan is “paid off,” you get the money

- Your payments are reported to the credit bureaus

It’s a safe way to build payment history without going into debt.

Step 5: Pay All Bills On Time—Always

Even if they don’t report to credit bureaus, missed bills can:

- Go to collections

- Hurt your credit indirectly

- Create financial stress

Pay on time every month. Use reminders or automation to help.

Step 6: Keep Credit Utilization Low

If your card limit is $500, aim to use no more than $150 at a time.

High balances hurt your score—even if you pay in full later.

Tips:

- Make multiple payments throughout the month

- Ask for a credit limit increase after 6 months

- Use the card for one small recurring bill (like Spotify) and pay it off

Step 7: Avoid Too Many Applications

Every time you apply for a new credit product, it creates a hard inquiry—which can slightly lower your score.

Too many applications = red flag for lenders.

👉 Only apply when necessary—and space them out over time.

Step 8: Check Your Credit Report Regularly

Use sites like:

- AnnualCreditReport.com

- Credit Karma (for score tracking)

- Your bank or credit card app (many offer free scores)

Look for:

- Errors

- Fraudulent accounts

- Unexpected collections

Dispute any mistakes immediately.

Step 9: Be Patient and Consistent

You won’t go from 0 to 800 overnight. But in 6–12 months, you can build a strong foundation.

Keep practicing:

- On-time payments

- Low credit use

- Smart financial habits

Over time, your credit will grow—and opportunities will follow.

Final Thoughts: Start Small, Grow Strong

Building credit is like planting a tree. At first, it feels slow. But with care and patience, it becomes something powerful that supports your entire financial life.

Start today—even with just one small step. Your future self will thank you.