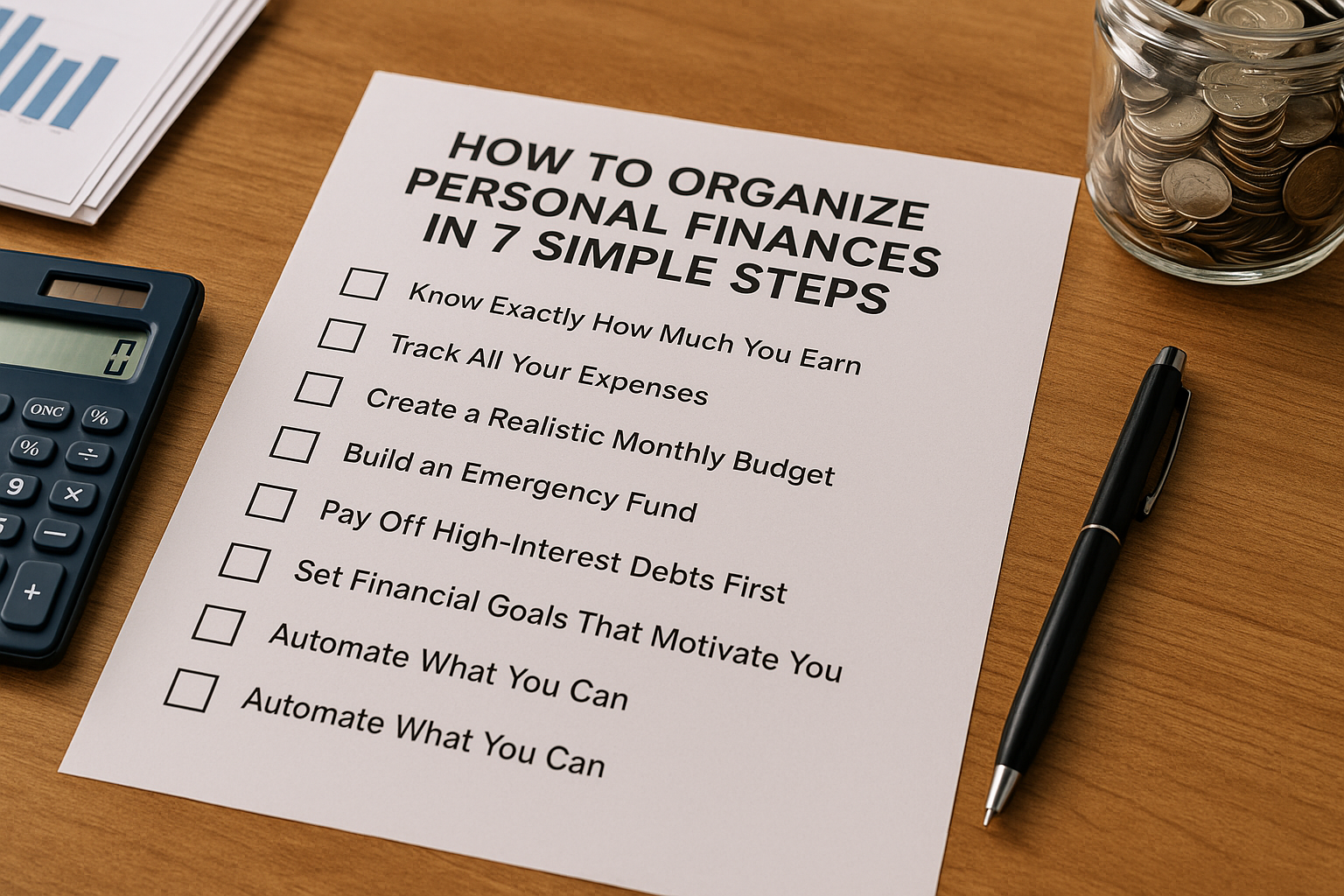

Managing money doesn’t have to be overwhelming. If you’re just starting your journey to financial freedom, organizing your personal finances is the first—and most crucial—step. With clear guidance and a solid plan, anyone can take control of their financial life. In this article, you’ll learn 7 simple and effective steps to help you organize your personal finances from scratch.

Step 1: Know Exactly How Much You Earn

It may sound obvious, but many people don’t actually know their real monthly income. Start by calculating your total income from all sources:

- Salary (after taxes)

- Freelance work

- Side hustles

- Passive income (e.g., interest or dividends)

Knowing your net income gives you a foundation to start planning.

Step 2: Track All Your Expenses

Before you can manage your money, you need to know where it’s going. Spend a month writing down every single expense, no matter how small. You can use:

- A notebook

- A spreadsheet

- Budgeting apps (like YNAB, Mint, or PocketGuard)

Categorize your spending (e.g., food, rent, transportation, entertainment) to identify your spending patterns.

Step 3: Create a Realistic Monthly Budget

A good budget is not about restricting yourself—it’s about being intentional with your money. Use your income and expenses to build a budget with categories like:

- Essentials (rent, food, transport)

- Savings

- Debt payments

- Discretionary spending (entertainment, dining out)

Apply the 50/30/20 rule if you’re unsure:

- 50% for needs

- 30% for wants

- 20% for savings or debt repayment

Budgeting apps can help automate this process.

Step 4: Build an Emergency Fund

Life is full of surprises. A sudden job loss, a medical emergency, or a broken car can ruin your finances if you’re unprepared. Start an emergency fund with the goal of saving at least 3 to 6 months of essential expenses.

If that feels too far off, start small:

- Save your change

- Set up an automatic transfer of $10 or $20 a week

- Keep it in a separate high-yield savings account

The key is to build a financial cushion that protects you from unexpected expenses.

Step 5: Pay Off High-Interest Debts First

Debt can be a major obstacle to financial stability, especially high-interest debts like credit cards. Use the avalanche method (pay off the highest interest rate first) or the snowball method (pay off the smallest balance first) to stay motivated.

Create a list of your debts with:

- Total amount owed

- Interest rate

- Minimum monthly payment

Focus your extra income toward one debt while making minimum payments on the rest.

Step 6: Set Financial Goals That Motivate You

You’re more likely to stick to a financial plan if you’re working toward something meaningful. Your goals might include:

- Saving for a vacation

- Buying a car or house

- Starting a business

- Building a retirement fund

Set SMART goals:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Break big goals into smaller milestones to track your progress and stay motivated.

Step 7: Automate What You Can

Automation is your best friend in personal finance. It helps you stay consistent and avoid forgetting important payments. Automate:

- Bill payments

- Savings contributions

- Debt repayments

- Retirement investments

This reduces mental effort and keeps you on track even when life gets busy.

Bonus Tips to Keep Going

- Review your budget every month. Adjust as needed.

- Avoid lifestyle inflation. Just because you earn more doesn’t mean you should spend more.

- Educate yourself. Read finance blogs, books, or listen to podcasts.

- Be patient. Financial growth takes time.

Final Thoughts: Start Simple, Stay Consistent

Organizing your personal finances isn’t something you do once—it’s a lifelong habit. But the earlier and more intentionally you start, the more empowered and secure your financial future will be.

Remember: You don’t need to be perfect—you just need to be consistent.