Freelancers, gig workers, commission-based professionals, and entrepreneurs all face a unique challenge: your income changes month to month. That makes budgeting and saving harder—but not impossible.

In this article, you’ll learn how to stabilize your financial life, even if your income is unpredictable.

Why Irregular Income Requires a Different Strategy

Most budgets are built around a steady paycheck. But when your income varies, you need to:

- Prioritize flexibility

- Prepare for slow months

- Avoid overspending during high-income months

- Protect your essentials no matter what

It’s not just about budgeting—it’s about buffering and planning ahead.

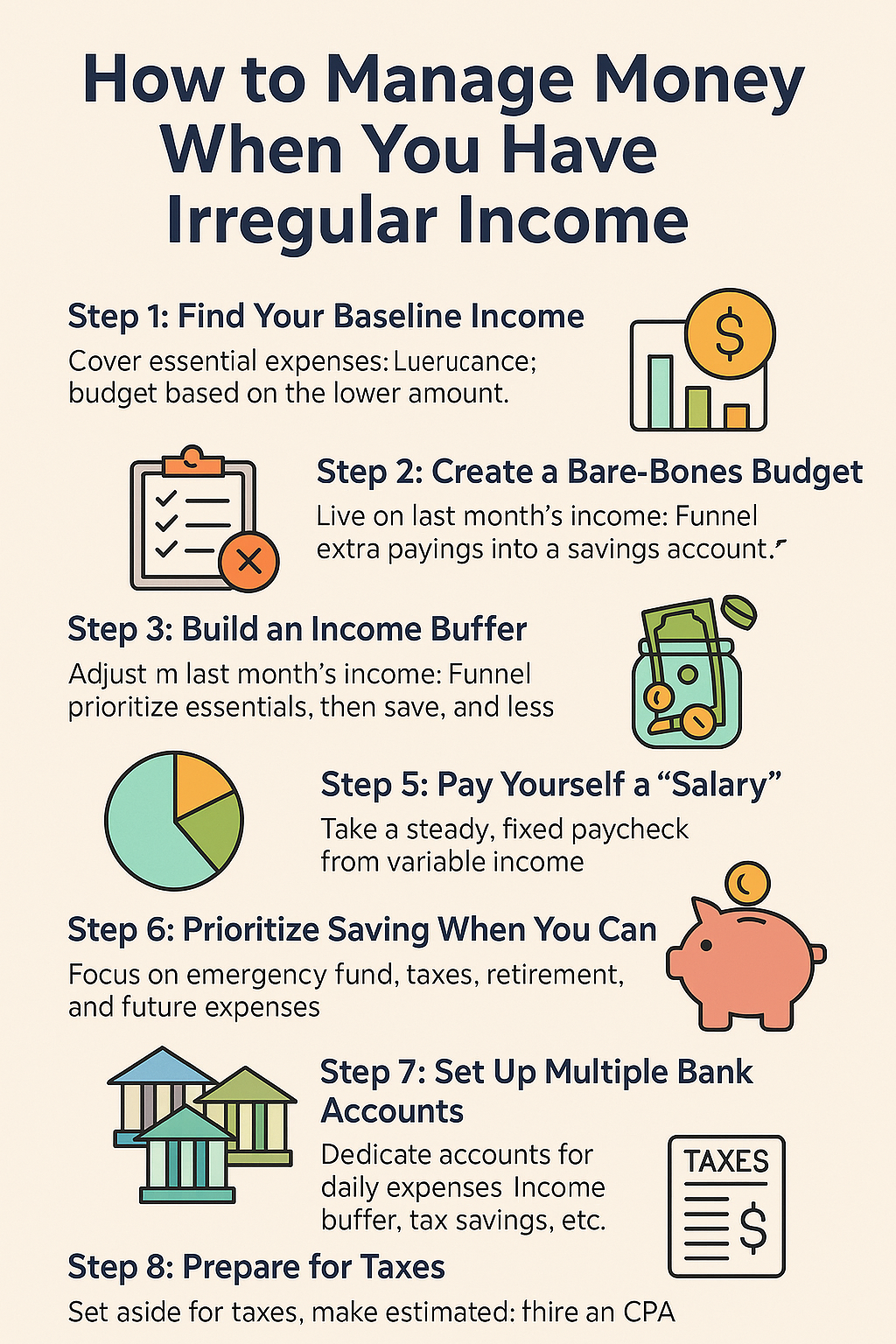

Step 1: Find Your Baseline Income

Review the last 6–12 months of income and calculate:

- Your average monthly income

- Your lowest monthly income

Your baseline income = your lowest reliable amount. This is the number you should budget around—not your best month.

👉 Example: If your income ranged from $2,000 to $4,500, budget based on $2,000.

Step 2: Create a Bare-Bones Budget

Build a “survival” budget that includes only essentials:

- Rent/mortgage

- Utilities

- Groceries

- Transportation

- Insurance

- Minimum debt payments

This is your minimum cost of living. During lean months, this budget keeps you afloat.

Step 3: Build an Income Buffer

Your goal is to always live on last month’s income.

Set up a separate savings account and funnel extra income into it during high-earning months.

Once you’ve saved up 1–2 months of expenses, you’ll have the cushion to smooth out fluctuations.

Step 4: Use a Variable Budget System

Adjust your budget each month based on expected income.

Try a tiered system:

- Tier 1: Essentials only (survival budget)

- Tier 2: Add savings, debt payments

- Tier 3: Add discretionary spending (fun, dining out, extras)

When income is low → Tier 1

When income is high → Tier 2 or 3

Step 5: Pay Yourself a “Salary”

Instead of spending all income as it comes in, pay yourself a fixed amount monthly or biweekly from your buffer.

Example:

- Income: $4,000 one month

- Pay yourself: $2,500

- Save the rest for low months

This creates predictability in your finances.

Step 6: Prioritize Saving When You Can

During good months, make saving a priority:

- Emergency fund

- Tax savings (especially if self-employed)

- Retirement accounts (like Roth IRA or SEP IRA)

- Future expenses (like car repairs, travel, etc.)

Aim to save at least 20–30% of variable income, depending on your situation.

Step 7: Set Up Multiple Bank Accounts

Separate accounts help with organization:

- Checking (daily expenses)

- Income buffer (acts like a paycheck)

- Emergency fund

- Tax savings

- Business expenses (if applicable)

Label them clearly to avoid confusion and overspending.

Step 8: Prepare for Taxes

If you’re self-employed or freelance, taxes are your responsibility.

- Set aside 25–30% of income for taxes

- Make quarterly estimated payments to avoid penalties

- Use tax software or hire a CPA for guidance

Don’t let tax season catch you by surprise.

Step 9: Use Tools That Support Irregular Income

Helpful tools:

- YNAB (You Need A Budget) – great for aging money and budgeting by category

- Goodbudget – uses envelope system

- Simple spreadsheets – customizable and low-cost

- QuickBooks Self-Employed – for taxes and business income tracking

Pick the system that fits your style and helps you stay consistent.

Final Thoughts: Flexibility Is Your Financial Superpower

Managing money on an irregular income is absolutely possible—you just need a strategy built for fluctuations, not perfection.

Create structure. Build buffers. Stay proactive. Over time, you’ll turn instability into confidence—and create financial peace no matter how unpredictable your income may be.