Your credit score affects more of your life than you might think. It can determine whether you’re approved for a loan, what interest rate you pay, if you can rent an apartment, or even land certain jobs.

If you’re new to the concept of credit, this article will explain what a credit score is, why it matters, and how to build and improve it—step by step.

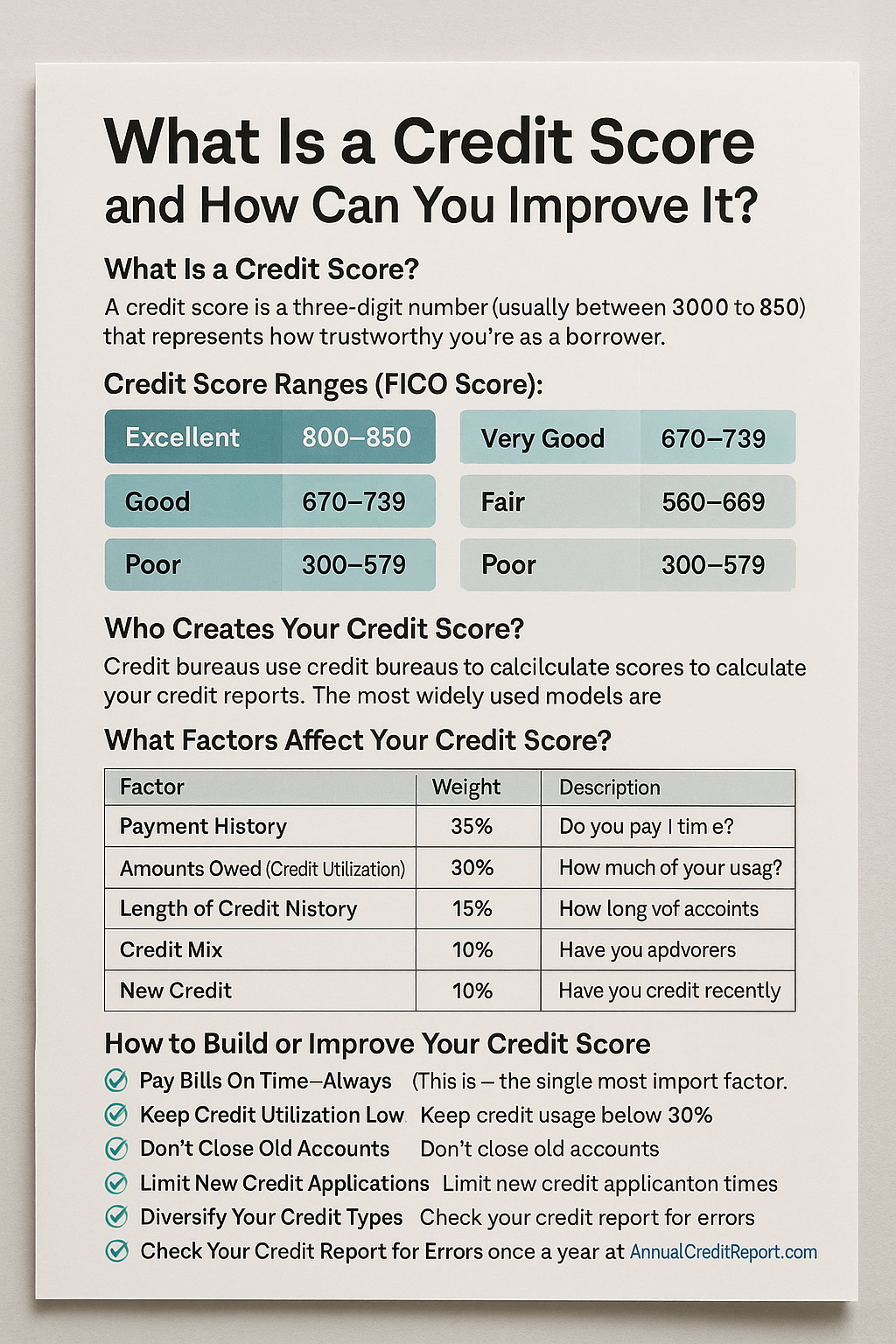

What Is a Credit Score?

A credit score is a three-digit number (usually between 300 and 850) that represents how trustworthy you are as a borrower. The higher the number, the more likely you are to be approved for credit—and get better terms.

Credit Score Ranges (FICO Score):

- Excellent: 800–850

- Very Good: 740–799

- Good: 670–739

- Fair: 580–669

- Poor: 300–579

Lenders, landlords, and even some employers use this score to assess financial responsibility.

Who Creates Your Credit Score?

In the U.S., your credit score is calculated by credit bureaus using data from your credit report. The main companies are:

- Equifax

- Experian

- TransUnion

The most widely used scoring models are:

- FICO Score (used by 90% of lenders)

- VantageScore

What Factors Affect Your Credit Score?

Here’s how a FICO Score is typically calculated:

| Factor | Weight | Description |

|---|---|---|

| Payment History | 35% | Do you pay your bills on time? |

| Amounts Owed (Credit Utilization) | 30% | How much of your available credit are you using? |

| Length of Credit History | 15% | How long have you had credit accounts? |

| Credit Mix | 10% | Do you have a variety of credit types? |

| New Credit | 10% | Have you applied for a lot of new credit recently? |

Why Does a Credit Score Matter?

A good credit score helps you:

- Get approved for credit cards and loans

- Secure lower interest rates (which saves money)

- Qualify for better rental and housing options

- Access higher credit limits

- Build financial independence

A poor credit score can lead to:

- Loan or card rejections

- Higher interest payments

- Bigger security deposits

- Difficulty renting an apartment

How to Build or Improve Your Credit Score

✅ 1. Pay Bills On Time—Always

This is the single most important factor. Late or missed payments can stay on your report for up to 7 years.

Set reminders, automate payments, and make minimum payments if that’s all you can afford.

✅ 2. Keep Credit Utilization Low

Try to use less than 30% of your total available credit. Even better: stay below 10%.

Example: If your credit limit is $1,000, keep your balance under $300.

✅ 3. Don’t Close Old Accounts

Even if you don’t use an old card often, keep it open if there’s no annual fee. Older accounts help your credit history length.

✅ 4. Limit New Credit Applications

Applying for several new credit accounts in a short time can hurt your score. Only apply when necessary.

✅ 5. Diversify Your Credit Types

A mix of credit cards, student loans, auto loans, or personal loans shows you can handle different kinds of debt.

Don’t take on debt just to improve your mix—but know that variety helps.

✅ 6. Check Your Credit Report for Errors

You can check your credit reports for free once a year at:

If you find errors (like wrong balances or missed payments), dispute them immediately. Mistakes can drag down your score.

How Long Does It Take to Improve a Credit Score?

- Paying bills on time? Improvements can be seen in 1–3 months

- Reducing credit utilization? Immediate impact once reported

- Removing negative marks? May take 6–12 months, or longer

- Building from scratch? Expect at least 3–6 months of responsible use

Tools That Can Help

- Credit Karma or Credit Sesame – Track your score for free

- Experian Boost – Add utility or streaming payments to your credit file

- Secured credit cards – Great for beginners or rebuilding credit

- Budgeting apps – Help prevent missed payments and overspending

Final Thoughts: Credit Is Power—If Used Wisely

Your credit score isn’t just a number—it’s a reflection of your financial habits. But the good news is: you’re in control.

Start small. Be consistent. Over time, your score will rise—and open doors to better financial opportunities.